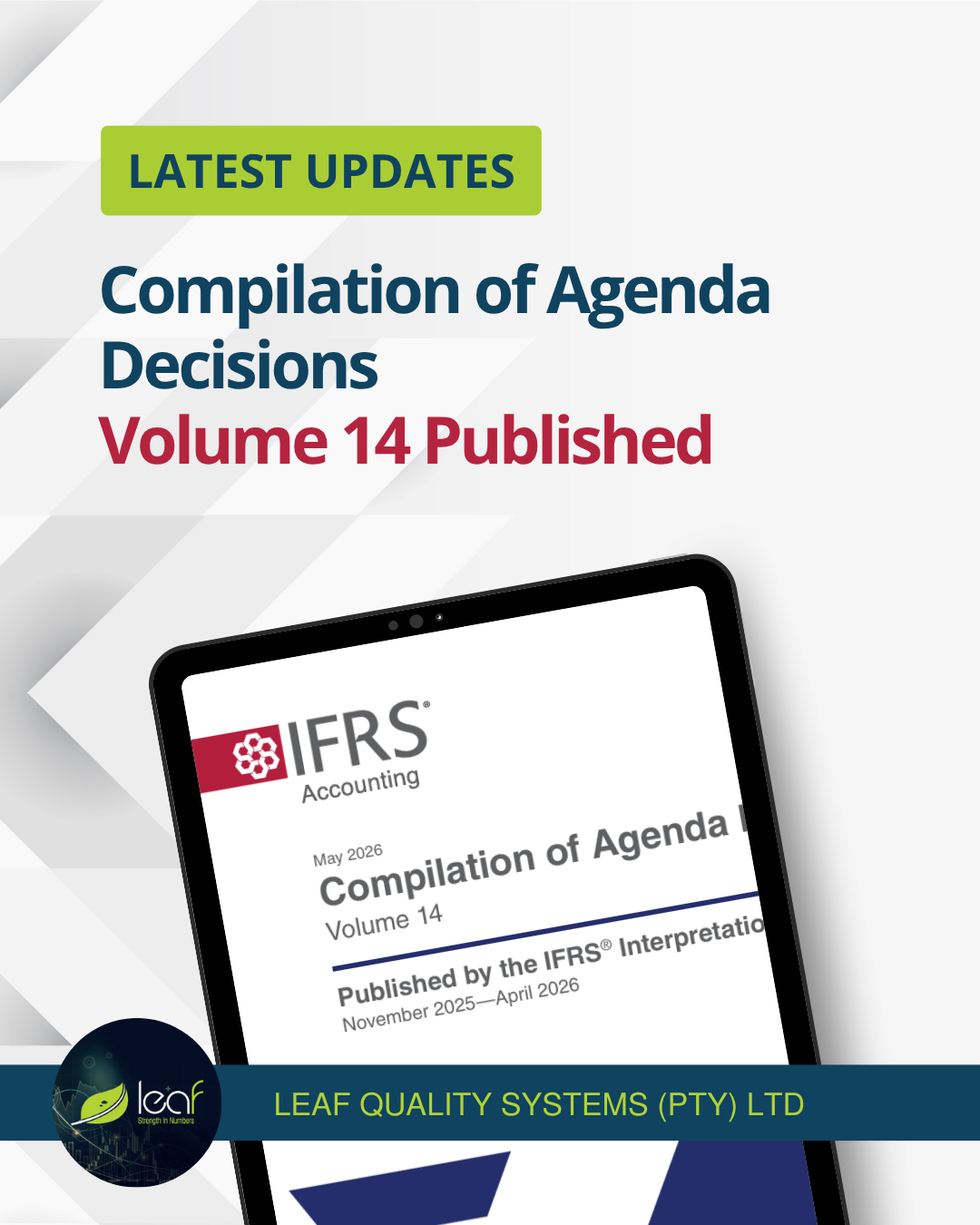

Exposure Draft Consolidation Exception Published by IASB

LEAF Quality Systems (Pty) Ltd2026-07-01T18:50:45+02:00LATEST UPDATE Exposure Draft Consolidation Exception In May 2026, the IASB published the Exposure Draft Consolidation Exception, which is available on: https://www.ifrs.org/content/dam/ifrs/project/ifrs-for-smes-accounting-standard-consolidation-exception/ed-iasb-sme-2026-1-consolidation-exception.pdf It addresses a question that was raised to the SMEIG and is open for comment until 9 September 2026, with more details on: https://www.ifrs.org/projects/work-plan/ifrs-for-smes-accounting-standard-consolidation-exception/ed-cl-consolidation-exception/ The application question was about whether the exception in paragraph 9.3 of the IFRS for SMEs Accounting Standard (Standard), from preparing consolidated financial statements (the ‘consolidation exception’), applies to an intermediate parent, if its ultimate (or intermediate) parent is an investment entity that produces separate financial statements in which [...]